fxcodebase-backup

Traders Dynamic Index Strategy

Source: https://fxcodebase.com/code/viewtopic.php?f=31&t=4134

Forum: 31 · Topic 4134 · 17 post(s)

Traders Dynamic Index Strategy

Nikolay.Gekht · Fri May 06, 2011 1:33 pm

Part I. Strategy

Here is a sample strategy developed on the base of the default Traders Dynamic Index indicator rules. Please see the indicator description for these rules.

Notes:

1) The strategy work on all types of the account: FIFO, non-FIFO and hedging.

2) The strategy supports as working on the closed bar as well as working on the active bar.

3) The strategy is supposed to work on particular account/instrument alone. No manual trading or other strategy must work on the same account/instrument. However, you can trade on other accounts or other instruments of the same accounts.

4) The strategy keeps one position in either long or short direction.

Important:

1) this strategy is a demo strategy and is NOT supposed to real trade.

2) when backtesting/optimizing/running strategy, please do not forget to set “Allow Trading” parameter to “Yes”. Otherwise the strategy will only show the alerts.

Download:

TradersDynamicIndexStrategy.lua

Please download and install the following indicators which are required to have the strategy properly working:

1) new version of the TradersDynamicIndex indicator: viewtopic.php?f=17&t=2069

2) Traders dynamic index interpreter indicator: viewtopic.php?f=17&t=4133

Please read the next topic in this post with analysis of the default parameters and brief optimization!

function Init()

strategy:name("Trades the Traders Dynamic Index Indicator data");

strategy:description("Implements scalping, active and moderate trading strategies for the Traders Index Indicator");

strategy.parameters:addGroup("Traders Dynamic Index Calculation");

strategy.parameters:addInteger("RSI_N", "RSI Periods", "Recommended values are in 8-25 range", 13, 2, 1000);

strategy.parameters:addInteger("VB_N", "Volatility Band", "Number of periods to find volatility band. Recommended value is 20-40", 34, 2, 1000);

strategy.parameters:addDouble("VB_W", "Volatility Band Width", "", 1.6185, 0, 100);

strategy.parameters:addInteger("RSI_P_N", "RSI Price Line Periods", "", 2, 1, 1000);

strategy.parameters:addString("RSI_P_M", "RSI Price Line Smoothing Method", "", "MVA");

strategy.parameters:addStringAlternative("RSI_P_M", "MVA(SMA)", "", "MVA");

strategy.parameters:addStringAlternative("RSI_P_M", "EMA", "", "EMA");

strategy.parameters:addStringAlternative("RSI_P_M", "LWMA", "", "LWMA");

strategy.parameters:addStringAlternative("RSI_P_M", "LSMA(Regression)", "", "REGRESSION");

strategy.parameters:addStringAlternative("RSI_P_M", "SMMA", "", "SMMA");

strategy.parameters:addStringAlternative("RSI_P_M", "WMA(Wilders)", "", "WMA");

strategy.parameters:addStringAlternative("RSI_P_M", "KAMA(Kaufman)", "", "KAMA");

strategy.parameters:addInteger("TS_N", "Trade Signal Line Periods", "", 7, 1, 1000);

strategy.parameters:addString("TS_M", "Trade Signal Line Smoothing Method", "", "MVA");

strategy.parameters:addStringAlternative("TS_M", "MVA(SMA)", "", "MVA");

strategy.parameters:addStringAlternative("TS_M", "EMA", "", "EMA");

strategy.parameters:addStringAlternative("TS_M", "LWMA", "", "LWMA");

strategy.parameters:addStringAlternative("TS_M", "LSMA(Regression)", "", "REGRESSION");

strategy.parameters:addStringAlternative("TS_M", "SMMA", "", "SMMA");

strategy.parameters:addStringAlternative("TS_M", "WMA(Wilders)", "", "WMA");

strategy.parameters:addStringAlternative("TS_M", "KAMA(Kaufman)", "", "KAMA");

strategy.parameters:addGroup("Levels");

strategy.parameters:addInteger("L1", "Low Level", "", 32, 0, 100);

strategy.parameters:addInteger("L2", "Middle Level", "", 50, 0, 100);

strategy.parameters:addInteger("L3", "High Level", "", 68, 0, 100);

strategy.parameters:addGroup("Price");

strategy.parameters:addString("TF", "Target Timeframe", "", "H1");

strategy.parameters:setFlag("TF", core.FLAG_PERIODS);

strategy.parameters:addString("T", "Target Price", "", "close");

strategy.parameters:addStringAlternative("T", "Open", "", "open");

strategy.parameters:addStringAlternative("T", "High", "", "high");

strategy.parameters:addStringAlternative("T", "Low", "", "low");

strategy.parameters:addStringAlternative("T", "Close", "", "close");

strategy.parameters:addStringAlternative("T", "Median", "", "median");

strategy.parameters:addStringAlternative("T", "Typical", "", "typical");

strategy.parameters:addStringAlternative("T", "Weighed", "", "weighted");

strategy.parameters:addGroup("Trading");

strategy.parameters:addInteger("S", "Strategy", "", 2);

strategy.parameters:addIntegerAlternative("S", "Scaliping", "", 0);

strategy.parameters:addIntegerAlternative("S", "Active", "", 1);

strategy.parameters:addIntegerAlternative("S", "Moderate", "", 2);

strategy.parameters:addInteger("BM", "Bar Mode", "", 0);

strategy.parameters:addIntegerAlternative("BM", "On Closed Bar", "", 0);

strategy.parameters:addIntegerAlternative("BM", "On Active Bar", "", 1);

strategy.parameters:addBoolean("AllowTrade", "Allow Strategy to Trade", "", false);

strategy.parameters:addString("Account", "Choose Account to trade on", "", "");

strategy.parameters:setFlag("Account", core.FLAG_ACCOUNT);

strategy.parameters:addInteger("Amount", "Trading amount (in lots)", "", 1, 1, 100);

strategy.parameters:addGroup("Alert");

strategy.parameters:addBoolean("ShowAlert", "Show Alerts", "", false);

strategy.parameters:addBoolean("PlaySound", "Play Sound", "", false);

strategy.parameters:addFile("SoundFile", " Sound File", "", "");

strategy.parameters:setFlag("SoundFile", core.FLAG_SOUND);

strategy.parameters:addBoolean("RecurrentSound", " Recurrent Sound", "", false);

end

local ShowAlert, PlaySound, SoundFile, RecurrentSound;

local AllowTrade, OfferID, AccountID, LotSize, Instrument;

local Price, ATDI, E, X;

local loaded = false;

local BarMode, LastSerial, first;

local name;

function Prepare(onlyName)

assert(core.indicators:findIndicator("TRADERSDYNAMICINDEX") ~= nil, "Please download and install TradersDynamicIndex.lua indicator");

assert(core.indicators:findIndicator("ANALYZETRADERSDYNAMICINDEX") ~= nil, "Please download and install AnalyzeTradersDynamicIndex.lua indicator");

assert(instance.parameters.TF ~= "t1", "The strategy cannot be applied on ticks");

assert(not(instance.parameters.PlaySound) or (instance.parameters.PlaySound and instance.parameters.SoundFile ~= "" and instance.parameters.SoundFile ~= nil), "The sound file must be chosen");

local sn;

if instance.parameters.S == 0 then

sn = "Scalping";

elseif instance.parameters.S == 1 then

sn = "Active";

else

sn = "Moderate";

end

name = profile:id() .. "(" .. instance.bid:instrument() .. "[" .. instance.parameters.TF .. "]" .. "." .. instance.parameters.T .. "," ..

sn .. "," ..

instance.parameters.RSI_N .. "," ..

instance.parameters.VB_N .. "," .. instance.parameters.VB_W .. "," ..

instance.parameters.RSI_P_N .. "," .. instance.parameters.RSI_P_M .. "," ..

instance.parameters.TS_N .. "," .. instance.parameters.TS_M .. ")";

instance:name(name);

if onlyName then

return ;

end

ShowAlert = instance.parameters.ShowAlert;

PlaySound = instance.parameters.PlaySound;

if PlaySound then

SoundFile = instance.parameters.SoundFile;

RecurrentSound = instance.parameters.RecurrentSound;

end

AllowTrade = instance.parameters.AllowTrade;

Instrument = instance.bid:instrument();

if AllowTrade then

AccountID = instance.parameters.Account;

Amount = instance.parameters.Amount * core.host:execute("getTradingProperty", "baseUnitSize", Instrument, Account);

OfferID = core.host:findTable("offers"):find("Instrument", Instrument).OfferID;

end

Price = core.host:execute("getHistory", 1, Instrument, instance.parameters.TF, 0, 0, true);

local pTDI = core.indicators:findIndicator("ANALYZETRADERSDYNAMICINDEX");

local p = pTDI:parameters();

p:setInteger("RSI_N", instance.parameters.RSI_N);

p:setInteger("VB_N", instance.parameters.VB_N);

p:setDouble("VB_W", instance.parameters.VB_W);

p:setInteger("RSI_P_N", instance.parameters.RSI_P_N);

p:setString("RSI_P_M", instance.parameters.RSI_P_M);

p:setInteger("TS_N", instance.parameters.TS_N);

p:setString("TS_M", instance.parameters.TS_M);

p:setInteger("L1", instance.parameters.L1);

p:setInteger("L2", instance.parameters.L2);

p:setInteger("L3", instance.parameters.L3);

p:setInteger("S", instance.parameters.S);

p:setString("T", instance.parameters.T);

ATDI = pTDI:createInstance(Price, p);

E = ATDI.E;

X = ATDI.X;

first = math.max(E:first(), X:first()) + 1;

BarMode = instance.parameters.BM;

end

function Update()

local period;

if not loaded then

return ;

end

period = Price:size() - 1;

if BarMode == 1 and period < first then

-- work on current bar, not enough data

return ;

end

if BarMode == 0 then

-- work on closed bar

if LastSerial == nil then

-- first tick received, ignore the current bar

LastSerial = Price:serial(period);

return;

elseif LastSerial == Price:serial(period) then

-- this bar has been already processed

return;

else

-- the first tick of a new bar

LastSerial = Price:serial(period);

period = period - 1;

end

end

ATDI:update(core.UpdateLast);

-- check exit condition

if X[period] > 0.1 then

-- exit long

ExitLong();

elseif X[period] < -0.1 then

ExitShort();

-- exit shorts

end

-- check entry codition

if E[period] > 0.1 and E[period - 1] <= 0 then

EnterLong();

elseif E[period] < -0.1 and E[period - 1] >= 0 then

EnterShort();

end

end

function ExitLong()

Alert("Exit Long", false);

if AllowTrade then

Exit("B");

end

end

function ExitShort()

Alert("Exit Short", false);

if AllowTrade then

Exit("S");

end

end

function EnterLong()

Alert("Enter Long", false);

if AllowTrade then

Exit("S");

Enter("B");

end

end

function EnterShort()

Alert("Enter Short", false);

if AllowTrade then

Exit("B");

Enter("S");

end

end

function Alert(msg, errorAlert)

if ShowAlert or errorAlert then

terminal:alertMessage(Instrument, instance.bid[NOW], name .. ":" .. msg, instance.bid:date(NOW));

end

if PlaySound and not errorAlert then

terminal:alertSound(SoundFile, RecurrentSound);

end

end

function Exit(side)

if not hasPosition(side) then

return ;

end

local msg, valuemap;

valuemap = core.valuemap();

valuemap.OrderType = "CM";

valuemap.OfferID = OfferID;

valuemap.AcctID = AccountID;

if side == "B" then

valuemap.BuySell = "S";

else

valuemap.BuySell = "B";

end

valuemap.NetQtyFlag = "y";

success, msg = terminal:execute(101, valuemap);

if not success then

Alert("Close Order Failed:" .. msg, true);

end

end

function Enter(side)

if hasPosition(side) then

return ;

end

local msg, valuemap;

valuemap = core.valuemap();

valuemap.OrderType = "OM";

valuemap.OfferID = OfferID;

valuemap.AcctID = AccountID;

valuemap.Quantity = Amount;

valuemap.BuySell = side;

success, msg = terminal:execute(100, valuemap);

if not success then

Alert("Open Order Failed:" .. msg, true);

end

end

function hasPosition(side)

local enum = core.host:findTable("trades"):enumerator();

local row;

while true do

row = enum:next();

if row == nil then

break;

end

if row.AccountID == AccountID and

row.OfferID == OfferID and

row.BS == side then

return true;

end

end

return false;

end

function AsyncOperationFinished(cookie, success, msg)

if cookie == 1 then

loaded = true;

elseif cookie == 100 then

if not success then

Alert("Open Order Failed:" .. msg, true);

end

elseif cookie == 101 then

if not success then

Alert("Close Order Failed:" .. msg, true);

end

end

end

The Strategy was revised and updated on January 21, 2019.

Part II. Parameters, Backtesting and Optimization

Nikolay.Gekht · Fri May 06, 2011 2:06 pm

Part II. Parameters, Backtesting and Optimization.

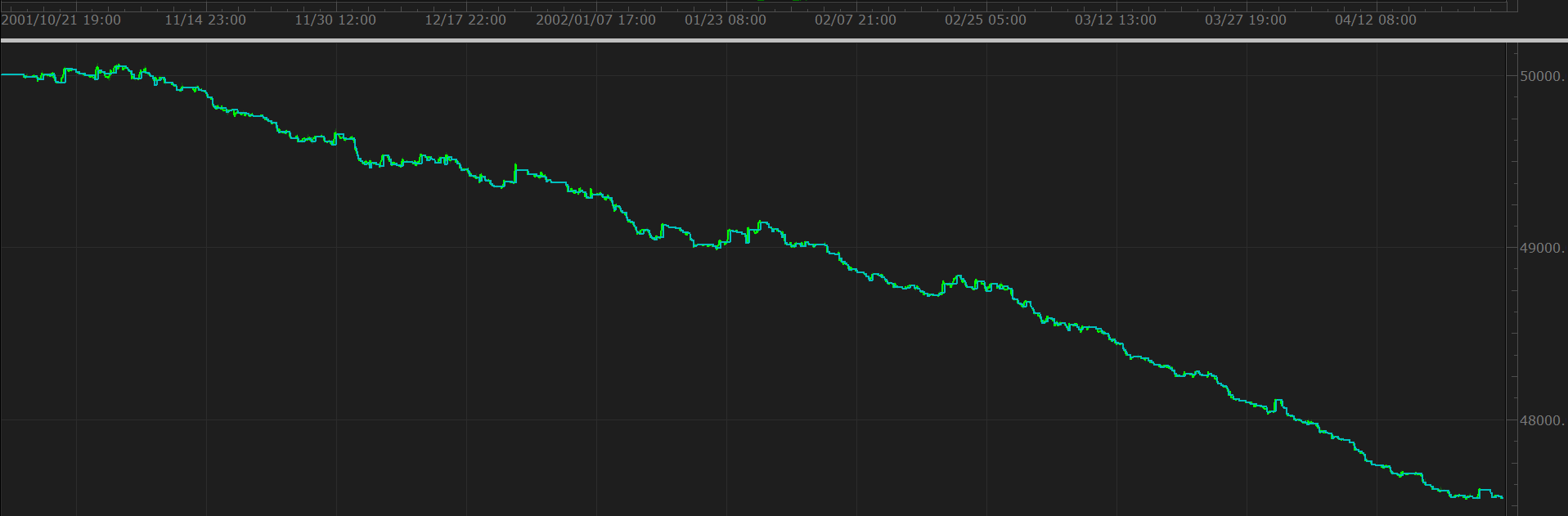

Used on small timeframes (m1-H1) the indicator result is not impressive at all:

(1-hour, default parameters, EUR/USD 2010 1-minute price archive)

However, all the examples of the strategies based on that indicator are usually demonstrated on 1-day timeframe:

(1-day, default parameters, EUR/USD 2010 1-minute price archive)

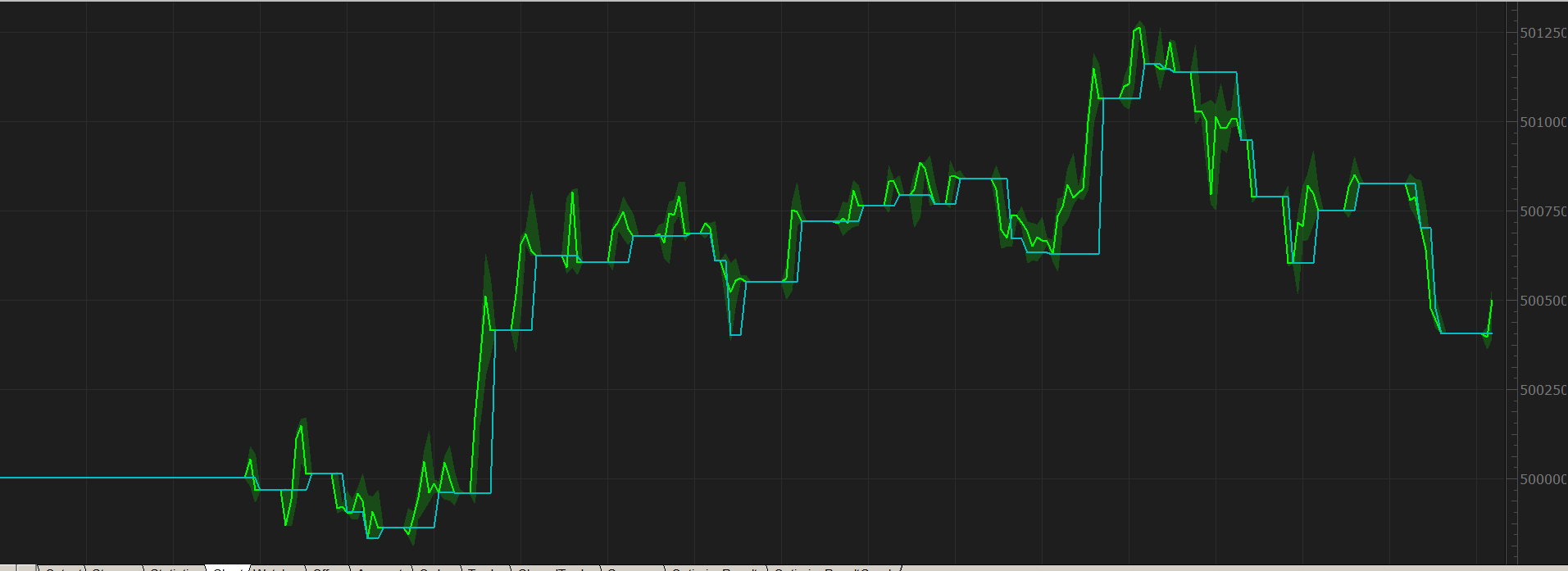

Of course, this does not mean that the indicator and strategy cannot be used for shorter time frame at all. The first attempt of the optimization shows that the problem is rather in the too short moving average applied to the RSI to get the price line:

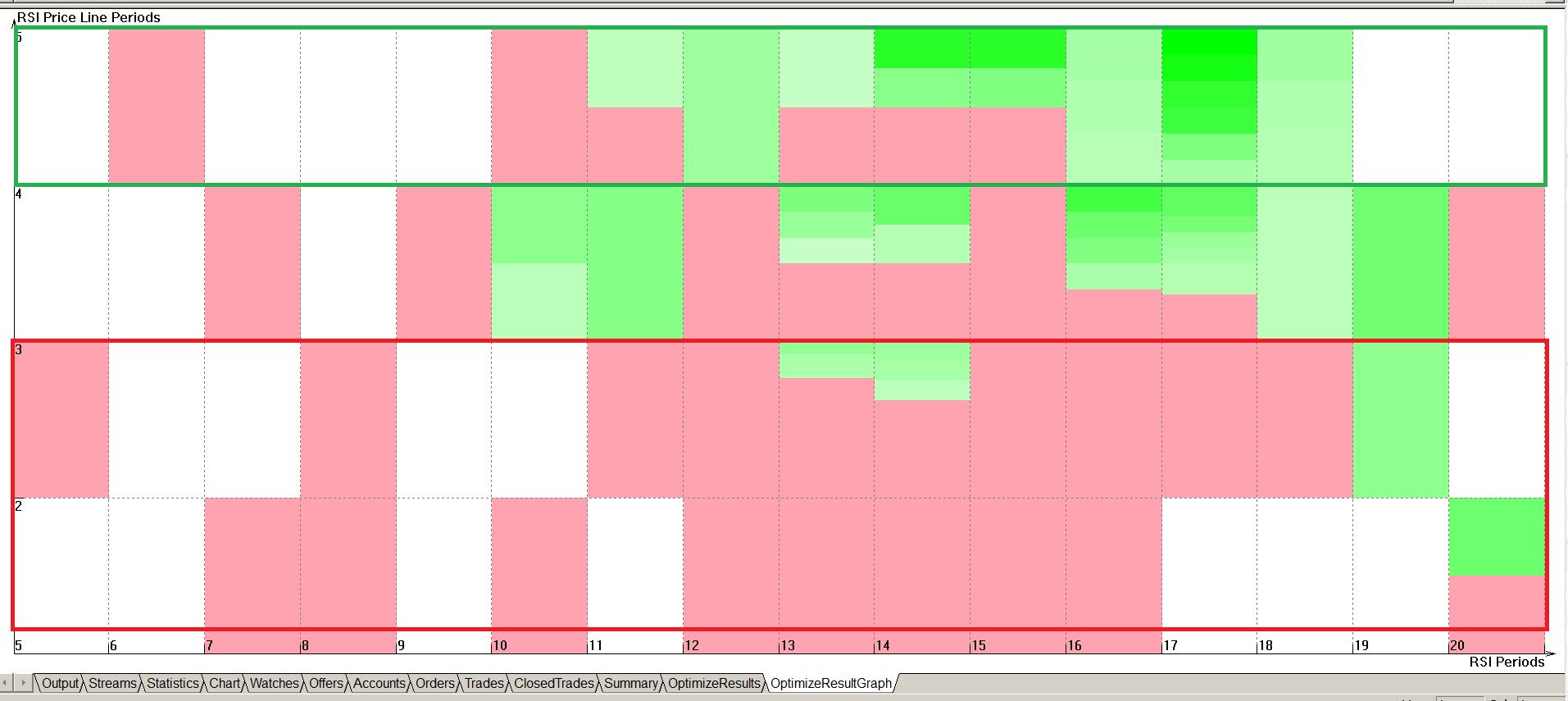

(optimization graph for EUR/USD 2010, 1-hour time frame. Map by RSI price line (Y) Signal Line (X) parameters).

RSI periods: 17 Vol.Band: 22 RSI Price Line: 5 Trade Signal: 8

We can get the equity curve which is more or less not so bad on EUR/USD 2010:

And even more or less works for the first four months of 2011:

Re: Traders Dynamic Index Strategy

Nikolay.Gekht · Fri May 06, 2011 2:09 pm

Want to backtest on the whole year data too? Heh!

1) Read articles here: http://fxcodebase.com/wiki/index.php/Ca … ndicoreSDK to find out how to backtest and optimize parameters using Strategy Debugger and how to get the 2001-2011 1-minute price archive.

2) Participate in the strategies backtesting and parameters optimizing.

Re: Traders Dynamic Index Strategy

Kingpin · Mon Jun 11, 2012 10:31 am

I get this error Message: “122: invalid account”

What is the reason for this and how could I solve this Problem?

Thx

Re: Traders Dynamic Index Strategy

jaricarr · Thu Nov 03, 2016 11:31 pm

Hello Nikolay,

Can you please add the exit criteria used in TTC TDI STRATEGY

http://fxcodebase.com/code/viewtopic.php?f=31&t=24914&p=42840&hilit=TRADERS+DYNAMIC#p42840

BUY ENTRY LEVEL BUY EXIT LEVEL SELL ENTRY LEVEL SELL EXIT LEVEL

Re: Traders Dynamic Index Strategy

Carbine · Sun Nov 13, 2016 8:07 pm

Kingpin wrote: I get this error Message: “122: invalid account”

What is the reason for this and how could I solve this Problem?

Thx

Hi, I’m also getting this error, any help would be appreciated!

Many Thanks

Re: Traders Dynamic Index Strategy

Apprentice · Mon Nov 14, 2016 4:16 am

Your request is added to the development list, Under Id Number 3672 If someone is interested to do this task, please contact me.

Re: Traders Dynamic Index Strategy

Apprentice · Mon Nov 14, 2016 4:26 am

Try it now.

Re: Traders Dynamic Index Strategy

Apprentice · Sun Dec 18, 2016 8:21 am

Strategy was revised and updated.

Re: Traders Dynamic Index Strategy

jaricarr · Tue Dec 20, 2016 11:53 pm

Hi Apprentice,

I re-downloaded the strategy. It still does not have the exit levels requested.

BUY ENTRY LEVEL BUY EXIT LEVEL SELL ENTRY LEVEL SELL EXIT LEVEL

Re: Traders Dynamic Index Strategy

jaricarr · Tue Dec 20, 2016 11:57 pm

Can you also add Vidya for RSI and Trade Signal Smoothing method please.

Re: Traders Dynamic Index Strategy

Apprentice · Thu Dec 22, 2016 1:44 pm

Your request is added to the development list, Under Id Number 3703 If someone is interested to do this task, please contact me.

Re: Traders Dynamic Index Strategy

papynou34 · Thu Nov 23, 2017 9:10 am

Hello All, Is it possible to forbidden the trading (open order) during some time zone? For example The startegy will not be allowed to trade during a zone from 22h00 to 23h00?

Thanks in advance for your answer

Re: Traders Dynamic Index Strategy

papynou34 · Tue Nov 28, 2017 6:27 am

Hello, Is it possible to add to this strategy a limit order and stop as precised in the picture?

Is it also possible to add a period for example from 17h00 to 17h30 where the tradinfg won’t be allowed?

Thanks in advance

Re: Traders Dynamic Index Strategy

Apprentice · Sun Dec 03, 2017 5:18 am

Your request is added to the development list under Id Number 3973

Re: Traders Dynamic Index Strategy

Apprentice · Thu Dec 07, 2017 5:22 am

Something like this?

TradersDynamicIndexStrategy.lua

Re: Traders Dynamic Index Strategy

papynou34 · Thu Dec 07, 2017 7:09 am

Hello Apprentice, This is more than perfect. A great Thanks to you. I will test it and let you know the result.